Make the Most of Your IRA and HSA Contributions Before Tax Day

With tax season fast approaching, now is an ideal moment to review your financial game plan—especially when it comes to maximizing contributions to your IRAs and HSAs. These accounts offer valuable...

Read more

Dividing Retirement Accounts After Divorce: 5 Tax Mistakes to Avoid for a More Secure Retirement

Avoiding Costly Tax Errors When Dividing Retirement Accounts in DivorceDivorce is one of the most financially complex transitions an individual can face. Along with dividing property, real estate,...

Read more

How to Choose the Right Financial Advisor: 5 Steps to Finding Your Best-Fit Advisor

Choosing the right financial advisor is a pivotal decision—one that can influence your retirement strategy, tax efficiency, investment outcomes, and long-term wealth preservation. With today’s...

Read more

What Adults With Student Loans Should Understand About Planning for Retirement

Managing Student Debt While Preparing for the FutureAcross the United States, two financial pressures weigh heavily on many adults: student loans and retirement savings. More than 43 million...

Read more

How to Build an Income Ladder Without Chasing Yield

Maximizing Your Retirement Income Strategy with Secure InvestmentsCreating a stable and predictable retirement income strategy without chasing high-yield, high-risk investments is both achievable...

Read more

Jump-Start Your Financial Health This January: A Practical Guide to Getting Back on Track

January is the perfect time to take a closer look at your finances and set the stage for a more intentional year. One of the most effective places to begin is by reviewing last year’s spending....

Read more

Step-Up in Basis: How Heirs May Reduce Capital Gains

Understanding Step-Up in BasisUnder tax law, the "step-up in basis" rule allows an inheritor to adjust the original value of an inherited asset to its market value at the time of the owner's death....

Read more

The First Five Years of Retirement: Taxes, Withdrawals, and Benefits

Understanding the Early Retirement LandscapeRetirees entering their first five years of retirement often encounter unique financial challenges. From adjusting to new spending patterns to organizing...

Read more

Asset Location 101: Improve After-Tax Returns Across Accounts

Optimize Your After-Tax Returns with Strategic Asset LocationAdvanced asset location strategies can significantly boost after-tax returns by strategically allocating investments across taxable, tax...

Read more

RMD Sequencing: Lower Taxes and Avoid Penalties

As retirees navigate their post-working years, managing Required Minimum Distributions (RMDs) becomes a critical task. Proper sequencing of RMDs can help minimize tax liabilities, manage Medicare...

Read more

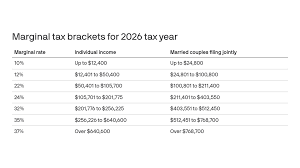

Understanding 2026 Tax Brackets and Strategic Planning

As we look ahead to 2026, major shifts are on the horizon for tax planning. The IRS recently released the official 2026 income tax brackets, reflecting changes implemented under the “One Big...

Read more

Should You Claim at 62, 67, or 70? A Timing Guide

Choosing the Right Age: Maximize Social Security BenefitDeciding when to claim Social Security benefits is a crucial decision that can impact your long-term financial stability. Considering...

Read more

Medigap vs. Medicare Advantage: Costs, Networks, and Tradeoffs

Understanding Your Options:Medigap vs Medicare AdvantageChoosing between Medigap and Medicare Advantage is a critical decision for retirees seeking to optimize their healthcare coverage. While both...

Read more

Don’t Let Outdated Beneficiaries Derail Your Estate Plan

One of the simplest yet most overlooked parts of estate planning is keeping your beneficiary designations up to date. Retirement accounts, insurance policies, and trusts all rely on beneficiary...

Read more

Open Enrollment Checklist for North Houston Retirees

Maximize Your Medicare: An Open Enrollment Checklist for Retirees in North HoustonAs open enrollment approaches, it’s crucial for retirees in North Houston to optimize their Medicare plans. This...

Read more

Fall Into Good Financial Practices For A Strong Year End

As the holiday season approaches, it's easy to feel overwhelmed by the hustle and uncertainty of your financial standing. But fear not! The crisp autumn air offers a perfect chance to hit pause,...

Read more

One Big Beautiful Bill Act: What You Need to Know

Understanding the One Big Beautiful Bill ActThe "One Big, Beautiful Bill" Act (OBBBA) isn't just a political catchphrase—it's a pivotal piece of legislation that brings both permanent and temporary...

Read more

End the Year Strong: 4 Key Financial Moves to Consider

The Clock is Ticking: Take Control of Your FinancesAs the end of the year draws near, it's the perfect moment to seize control of your financial planning. We understand that financial tasks can...

Read more

National Annuity Awareness: Securing Your Future

June Celebrates National Annuity Awareness MonthWith June marking National Annuity Awareness Month, it's a perfect time to explore how annuities could be a pivotal part of your retirement planning....

Read more

Social Security Fairness Act: What Retirees Need to Know

The Significance of the Social Security Fairness ActOn January 5, 2025, a monumental change occurred in the landscape of retirement benefits with the signing of the Social Security Fairness Act....

Read more

Timing is Key: Understanding RMDs in a Market Slump

Roth Conversion and TimingWith the market down, some individuals might see the present time as an opportunity to expedite Roth conversions. However, they must remember the sequence: RMDs must be...

Read more

2025 Update: New Rules for Inherited IRAs

Staying informed about retirement account rules is crucial for beneficiaries, particularly as regulations continue to evolve. One area that has caused confusion is the handling of Required Minimum...

Read more

Understanding Risk Tolerance for Smarter Investments

Discovering Your Comfort with Risk: A Crucial Investment StepWhen it comes to managing investments, knowing your risk tolerance is not just beneficial—it's essential. Balancing the opportunity for...

Read more

Understanding Tax Benefits and Implications of Homeownership

Beyond the pride of owning a home, there are significant financial benefits that come with it, especially during tax season. As a homeowner, navigating these benefits can feel overwhelming due to...

Read more

Exploring Charitable Giving Options for Maximum Impact

Charitable Giving Options: Make a Greater ImpactPhilanthropy isn't just about money—it's about making a positive impact on the world and experiencing the satisfaction that comes from giving back....

Read more

Key Considerations for Roth Conversions

Understanding Roth Conversions: Important ConsiderationsWhen it comes to retirement planning, one of the strategies that often pops up is the Roth conversion. The decision to convert traditional...

Read more

Navigating Missed RMDs: A Step-By-Step Approach

Fixing a Missed RMD in 5 Easy StepsRequired Minimum Distributions (RMDs) are mandatory withdrawals you must take from your Individual Retirement Accounts (IRAs) under certain conditions. Depending...

Read more

Understanding Risk Tolerance for Smarter Investments

Discovering Your Comfort Zone: Navigating Risk Tolerance Investing can be a thrilling yet daunting endeavor, as balancing opportunities with their potential losses is inherently challenging. Our...

Read more

IRA New Year's Resolutions for a Financially Secure Future

As the new year unfolds, it's the perfect time to revisit our financial goals and commitments. A crucial aspect of financial planning involves managing your Individual Retirement Accounts (IRA)...

Read more

View more